Equations of Production

What prevented the classical authors from seeing that the theory of value and distribution could be firmly grounded in the concept of physical real cost? Given their primitive tools of analysis, they did not see that the information about (1) the system of production actually in use and (2) the quantities of the means of subsistence in support of workers was all that was needed in order to determine directly (without any need to go through labour values) the system of necessary prices and the general rate of profits.

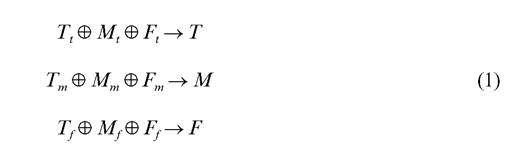

This Sraffa understood as early as November 1927, as we can see from his hitherto unpublished papers kept at Trinity College Library, Cambridge (UK), with respect to what he called his “first” (without a surplus) and “second equations” (with a surplus); see Kurz (2012).We may illustrate his argument by starting from James Mill’s above case with three types of commodities - tools (t), raw materials (m), and the food of the labourer (f). Production in the three industries may then be tabulated in the following way:

Here Ti, Mi and Fi designate the inputs of the three commodities (employed as means of production and means of subsistence) in industry i (i = t, m,f), and T, M and F total outputs in the three industries; the symbol “{” indicates that all inputs on the left-hand side (LHS) of “s”, representing production, are required to generate the output on its right-hand side (RHS). Adopting the terminology of the classical authors, Sraffa calls these relations “the methods of production and productive consumption” (Sraffa 1960: 3). In the hypothetical case in which the economy is just viable, that is, able to

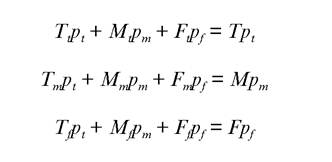

From this schema of reproduction and reproductive consumption we may directly derive the corresponding system of “absolute” or “natural” values, which expresses the concept of physical real cost-based values in an unadulterated way.

Denoting the value of one unit of commodity i by pi (i = t, m, f), we have:

Since only two of the three equations are independent of one another, fixing a standard of value, whose price is ex definitione equal to unity, provides an additional equation without adding a further unknown and allows one to solve for the remaining dependent variables.

The reasoning up until now shows that there is no need whatsoever to invoke labour values. In fact, it would not be clear what could be meant by them vis-a-vis the undeniable heterogeneity of labour performed in the different lines of production. Also, with regard to the next stage, which refers to a system with a surplus and given commodity (or real) wages advanced at the beginning of the production period, the same applies: information about the system of production in use and real wages is all that is needed in order to ascertain relative prices and the additional variable that reflects the distribution of the surplus product in conditions of free competition: the general rate of profits. This rate applies to the values of the “capitals” advanced in the different industries by capitalists.

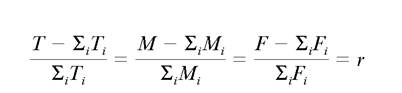

We start once more from the system of quantities consumed productively and produced (1), but now we assume that where at

where at

least with regard to one commodity the strict inequality sign applies. In the extremely special case of a uniform rate of physical surplus across all commodities, as it was contemplated by such diverse authors as Ricardo, Torrens, and John von Neumann (1945), we have:

In it the general rate of profits, r, equals the uniform material rate of produce. As Sraffa emphasized, here we see the rate of profits in the commodities themselves as having nothing to do with their values.

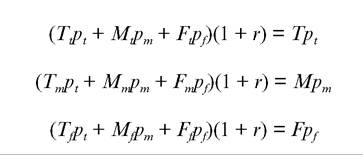

However, in general the rates of physical surplus will differ as between different commodities (and some of these rates might even be negative).Yet, unequal rates of commodity surplus do not, by themselves, necessarily imply unequal rates of profit across industries. In conditions of free competition the concept of “normal” prices (Smith, Ricardo), or “prices of production” (Torrens and Ricardo), implies that the social surplus is divided in such a way between the different employments of capital that a uniform rate of profits obtains. This condition is met by the following system of production equations:

These three equations are independent of one another. Fixing a standard of value provides a fourth equation and no extra unknown, so that the system of equations can be solved for the dependent variables: the general rate of profits and prices.

This result is startling and implicitly puts in sharp relief the shortcomings of some received economic doctrines. To see its far-reaching implications we turn to the way in which Sraffa introduces it right at the beginning of his 1960 book. With the real wage rate given and paid at the beginning of the periodical production cycle, the problem of the determination of the rate of profits consists in distributing the surplus product in proportion to the capital advanced in each industry. Clearly, Sraffa observes,

such a proportion between two aggregates of heterogeneous goods (in other words, the rate of profits) cannot be determined before we know the prices of the goods. On the other hand, we cannot defer the allotment of the surplus till after the prices are known, for... the prices cannot be determined before knowing the rate of profits. The result is that the distribution of the surplus must be determined through the same mechanism and at the same time as are the prices of commodities. (Sraffa 1960: 6, emphasis added)

This passage shows that the concept of “capital” as a magnitude that can be known prior to and independently of the prices of commodities and the rate of profits (the rate of interest) cannot generally be sustained.

We encounter a variant of this concept in Marx’s labour value-based reasoning, another in the marginalist concept of a given “quantity of capital”. Marx attempted to determine the general rate of profits and prices of production in two steps, which Ladislaus von Bortkiewicz (1906-07, essay II: 38) aptly dubbed “successivist” (as opposed to “simultaneous”). In a first step Marx assumed that the general rate of profits is determined independently of, and prior to, the determination of prices as the ratio between the labour value of the social surplus and that of the social capital, consisting of a “constant capital” (means of production) and a “variable capital” (wages or means of subsistence). In a second step he then used the rate of profits ascertained in this way to calculate prices. Underlying his approach is the hypothesis that while the “transformation” of values into prices is relevant with regard to each single commodity, it is irrelevant with regard to commodity aggregates, such as the surplus product or the social capital, and the ratio of such aggregates. Yet this is not generally the case: the value of the sum total of heterogeneous capital goods (as well as the value of the sum total of the commodities forming the surplus product) cannot be taken as given and independent of the rate of profits, but has to be determined simultaneously with the rate of profits.

More on the topic Equations of Production:

- Equations of Production

- Production, capitalization and money

- Production Prices with Oil and the Metaphor of the Snapshot

- Writing the Equations: Garegnani’s View

- The Spring of Sraffa’s Equations: The “absolutely necessary commodity” and the “community that produces just what is sufficient to keep it going”

- Production of Commodities by Means of Commodities

- Dmitriev and Bortkiewicz

- The Wage Curve

- Choice of Technique

- The capitalist law of exchange