Back to a Surplus Theory of Interest

The conception of economic activity as a circular flow and the “surplus approach” to interest surfaced again at the turn of the nineteenth century, especially in Germanspeaking countries, partly in opposition to marginal productivity theories.

A leading figure was Friedrich von Wieser, Bohm-Bawerk’s colleague and brother in law. He adopted a view of production as a circular flow right from his Ursprung of 1884, maintaining that unidirectional production is characteristic of primitive societies, whereas circular production pertains to developed societies (Wieser 1884: 50; see Kurz and Sturn 1999: 83). In his more mature work (Wieser 1889), he built on the observation that there is simultaneously a certain consumption of means of production, and a certain production of them, with a positive surplus. In value terms (irrespective of the price theory adopted) “the subtrahend is somewhat less than the minuend, and the required residue of interest must be the result” (Wieser 1889: 142; see Opocher 2005). More generally, he was convinced that the “imputation” of output to each factor should be ascertained not using marginal variations, but under the assumption of undisturbed, actual input use (see Rothschild 1973) and that such an imputation is the solution of a system of equations. Vladimir Karpovich Dmitriev (1904 [1974]) and Ladislaus von Bortkiewicz (1906— 07 [1952]) also tried to explain interest on the basis of a given system of production, even though they started from unidirectional processes of finite length, like the leading Austrians (see Kurz and Gehrke 2006: 115-16, n. 22): implicit in a system of production there was a rate of interest, which can be calculated on the basis of a mathematical description of all the economic processes in use.The main formal contribution, however, is that of von Neumann. He presented a theory of interest in an economy in which “goods are produced...

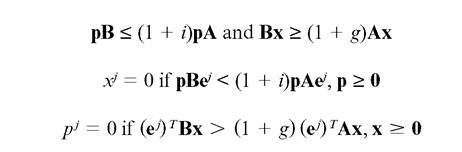

in the first place from each other” (Neumann 1937 [1945-46]: 1) in conditions of constant returns to scale; differently from Dmitriev and Bortkiewicz, and, like Wieser, he considered reciprocal inputoutput relations. He introduced technological alternatives in each sector and universal joint production (which includes fixed capital as a special case), in the sense of a finite number of potential processes. Accordingly, the determination of the rate of interest and of relative prices is placed in the framework of a wider problem of the choice of technique and optimization in which also the rate of economic expansion and the activity levels are determined. This has been an important development, since Wieser had been criticized for his failure to explain how input choices come about (see Wicksell 1893 [1954]: 24-5). His model follows a general equilibrium logic, but marginal productivities, preferences, and factor supplies have no role in it. Assuming m processes and n goods, let A be the n ? m matrix of input coefficients when processes are run at unit level; likewise, let B be the n ? m matrix of output coefficients. The net profit from each process, evaluated at price vector p, is [pB - (1 1 i)pA]. The total balance of each commodity, calculated at activity levels x, is [Bx - (1 + g)Ax], where (1 + g) is the growth factor. It is assumed that no process can make positive net or extra profits and that no commodity can be produced short of its use; that a process, which makes losses, is not activated and that a good produced in excess has a zero price. Hence, denoting by e the jth unit vector, we have:

Equilibrium is determined as a pair of vectors (p, x) and of scalars (i, g) satisfying the above inequalities: it is shown that, on the assumptions employed by von Neumann, the solution is a saddle point where g = i.

A similar logic, it must be briefly said, can also be applied to the determination of the rewards of primary factors available in fixed supply, as in Knight (1925), Samuelson (1958), Uzawa (1958) and Dorfman et al.

(1958). Wieser, again, is credited with having had an inspiring role in it. Activity levels and factor prices are determined by a system of inequalities in which the value of production (at any given vector of commodity prices) is maximum and the cost of employing the available factors is minimum. A fact that has attracted the interest of some authors is that in this model one can define a “purely physical quasi-social marginal productivity” (Samuelson 1958: 315) of each factor (by marginally changing its supply) and that in equilibrium this equals the real reward of this factor (Knight’s theorem).About ten years before von Neumann, Piero Sraffa explored the idea that socio- technical conditions alone may suffice to determine simultaneously the rate of profits (interest) and relative prices as solutions of a system of equations. This has been part of an ambitious project of rethinking the old problems of value and distribution paving the ground for new analytical solutions, which will be completed in Sraffa (1960). What are now known as Sraffa’s “second equations” (see Kurz and Gehrke 2006 for details) were drafted in 1928 (the 1927 “first equations” referring to the limiting case of production without a surplus). Sraffa assumed, like von Neumann after him, that the production of each commodity required the consumption of several commodities, either as means of subsistence of workers or as means of production, and that there was an overall surplus of some (or all) commodities and a deficit of none. For each commodity, the value of the output should be equal to the value of all the commodities consumed plus a profit (interest) component, at a uniform rate. Denoting now by A the square matrix of all material inputs per unit of output (as calculated at specific output levels), including workers’ sustenance, we have:

All depends on the properties of matrix A: the equilibrium vector of commodity prices is an eigenvector of A, while the profit (interest) factor (1 + i) is the reciprocal of the dominant eigenvalue.

By the Perron-Frobenius theorems of linear algebra, there is a unique largest eigenvalue, associated with an eigenvector with positive elements, which is unique up to a scalar factor. A solution therefore exists if the dominant eigenvalue is lower than one. (The Perron-Frobenius theorems are central for Sraffa’s theory of distribution just as Euler’s theorem was central for Wicksteed’s theory and it is curious to note that none of them appeared to know the relevant mathematical theorem, but both were able to “see” the necessity for them and had been assisted for a proof by a mathematician, Frank P. Ramsey and John Bridge, respectively.)As in the case of von Neumann’s model, labour and wages do not appear explicitly: they are “mixed together” by the assumption that a unit of labour receives the anticipation, not of a wage of a certain value, but of an “inventory” of commodities. It follows that an increase, say, in the amounts forming this inventory or an increase in the amount of labour per unit of output in all sectors are indistinguishable: both determine an increase in the consumption of commodities per unit of output and a fall in the rate of profits (interest). This is quite consistent with the main conclusions that Ricardo reached in his “corn model”.