Michal Kalecki is certainly one of the most enigmatic economists of the twentieth century.

Besides anticipating Keynes’s General Theory (1936) he is credited with paving the way for connecting imperfect competition to business-cycle analysis, designing the first macro-dynamic model unifying mathematics, statistics, and economic theory, as well as developing a theory of the political business cycle (Lopez and Assous 2010; Toporowski 2013).

Michal Kalecki was born on 22 June 1899 in Lodz into a Polish-Jewish family, and died in Warsaw on the 17 April 1970. He began mathematical studies in 1917 - going on to publish several papers in that field - at the Warsaw University and later studied civil engineering at the Gdansk University Engineering College. In 1923, because of the failure of his father’s cotton business, Kalecki interrupted his studies and decided to work for a credit rating agency. It was then that he started working on economic problems. At the same time, his socialist political inclinations led him to study Marx’s Capital (1976) as well as the works of Rosa Luxemburg and Mikhail Tugan-Baranovsky. In the late 1920s, he started contributing regularly to two Polish economics journals, denying in several articles the existence of self-correcting market mechanisms likely to eliminate mass unemployment, and arguing that the way to escape from crises was by stimulating aggregate demand.

Thanks to his mathematical and economics background, Kalecki obtained his first academic job at the Institute for the Study of Business Cycles and Prices in late 1929. His task was twofold. With Erik Landau he produced the first estimates of prices, investment, consumption and social income in Poland; meanwhile, Kalecki also focused on crafting a formal mathematical treatment of the business cycle. In July 1933, he published a booklet entitled An Essay in the Theory of the Business Cycle in which he attempted to explain observed cycles with a system whose solutions are deterministic cycles.

This contribution constitutes an important step in the history of macroeconomics. For the first time, the functioning of a constrained demand economy had been described mathematically and estimated statistically.In 1936, thanks to a Rockfeller scholarship, he went to Sweden, Norway and then England. From there, Kalecki established scholarly contacts with Bertil Ohlin, Erik Lindahl, Tjalling Koopmans, Ragnar Frisch, Piero Sraffa, Richard F. Kahn, John Maynard Keynes and Joan Robinson. In the same year, he embarked on the supervision of the Cambridge Research Scheme of the National Institute of Economic and Social Research into Prime Costs, Proceeds and Output. During the Second World War, he moved to the Oxford University Institute of Statistics. In March 1945, he left for Montreal to take a post at the International Labour Office before in 1946 taking a position as Assistant Director in the Department of Economic Affairs of the United Nations Secretariat, in New York City. His work, set out in the World Economic Report series, was mainly dedicated to the study of problems of full employment and inflation in both developed and underdeveloped countries, including the socialist ones.

In 1954, Kalecki resigned in protest against the McCarthyism which swept the United Nations secretariat. At the end of February 1955, he returned to Poland where, after the death of Stalin, the political situation had become more positive. During the period up until the beginning of 1960, he served as an adviser on matters concerning economic

planning, and during 1958 and 1959 was especially deeply involved in the Outline Perspective Plan for the years 1961-75. However, this plan was severely criticized for departing from the communist orthodoxy as regards, in particular, the relative size of consumption and investment. At the same time, Kalecki was very active in teaching and research at the Polish Academy of Sciences. In 1961 he began lecturing at the Central School of Planning and Statistics, where he eventually took a full-time job.

Kalecki and Underemployment Equilibrium

Kalecki’s argument regarding the functioning of a constrained demand economy had two strands. The first was an explanation of why, for a given capital stock and given money wages, the economy can become stuck in a stable short-period equilibrium with unemployment. The second was an explanation of why, when the capital stock and money wages are variable, the economy is bound to fluctuate.

Kalecki’s first point serves to deny the existence of self-correcting market mechanisms which would eliminate excess supplies of productive resources. Moreover, he denied that these would exist even in a competitive economy. Joan Robinson claimed that it was precisely because Kalecki had remained outside the mainstream of traditional economics that he succeeded in developing a new macroeconomic analysis (see, for example, Robinson 1966). She maintained that Kalecki, unlike Keynes, did not have to free himself from the mainstream theoretical framework, simply because he did not know it. However, a close look at his 1934 paper “Three systems” reveals that he was indeed familiar with important authors of both the Marshallian and Wicksellian traditions, as well as business-cycle theorists such as Albert Aftalion and Joseph Schumpeter.

According to Kalecki, there are theoretically conceivable circumstances in which, with fixed money wages and a constant capital stock, the economy will become stuck in a “quasi-equilibrium” with mass unemployment. The essence of Kalecki’s theory of employment consists in a distinction between endogenous components of aggregate demand (for example, worker’s consumption) and exogenous components (for example, investment outlays, exports surpluses, budget deficits). Along these lines, in a model that integrates the real and monetary sectors of the economy, Kalecki (1934) demonstrates that any disequilibrium between aggregate demand and aggregate supply causes a change in output (and hence income), which leads the economy to an equilibrium position.

A crucial assumption of both Keynes’s and Kalecki’s analysis is that the marginal propensity to spend is less than one. Therefore Patinkin’s claim that Kalecki had not anticipated Keynes’s central message has to be rejected (Chapple 1995; Assous 2007).However, even if a demand-constrained economy behaves differently from an economy in which Say’s law applies, the proof of the possibility of a continuum of equilibriums parameterized by a given money wage does not suffice in itself to demonstrate the possibility of persistent unemployment. His point was that to show that unemployment is persistent, it is necessary to resort to dynamic analysis. He thought the phenomena of underemployment had to be considered as a case of disequilibrium dynamics.

Kalecki described a mechanism showing that the real equilibrium of the economy is not independent from the level of money wages and prices. This adjustment mechanism was the so-called Keynes effect (Leijonhuvfud 1968), by which a lower price level increases the real money supply and so lowers the interest rate, and then stimulates investment until, through a multiplier effect, income and production reach a level that ensures an equilibrium in all markets.

Realizing that equilibrium analysis and comparative statics are not the best tools for demonstrating the possibility of mass unemployment, Kalecki developed a double argument. He first emphasized that the adverse effect of lower prices on debtors via an increased real debt burden can provoke bankruptcies and lead ultimately to lower aggregate demand because debtors have a higher propensity to spend than do creditors. Second, deflation generates expectations of falling prices and lower future prices which materialize in a higher real rate of interest and thus lower spending. Unlike Keynes, Kalecki was ready to accept that this last argument matters only during the adjustment process: “your point on the rising real rate of interest is valid only in the period of adjustment.

Once a new equilibrium is achieved the wages and prices stop falling” (Kalecki 1944 [1990]: 568). From that point of view, Kalecki’s employment theory is more in line with the dynamic Keynesian approach later developed by Tobin (1975) than with the static Keynesian analysis of Hicks (1937) and Modigliani (1944).Imperfect Competition, Income Distribution and the Multiplier Analysis

From 1936, Kalecki (1936) resorted exclusively to imperfect competition. Initially, in reference to Edward Chamberlin’s framework (1933), his purpose was to clarify the problem of the micro foundations of the General Theory, in which Keynes considered the degree of competition as one of the “givens” for the determination of the levels of employment and output.

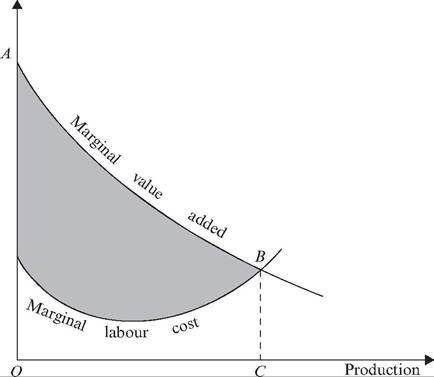

The macro equilibrium is shown in a figure presenting micro curves, which are summed to bring about the macro aggregates. Each imperfectly competitive firm produces so as to equate the marginal “value added” and marginal cost. The marginal “value added” curve is the marginal revenue curve of any firm, given the conjecture the other firms’ prices are given. The intersection of the curves of marginal revenue and marginal cost is thus a representation of profit maximization. Once the costs of material inputs are deduced from both curves, we obtain Kalecki’s figure (Figure 7).

In the labour market, workers are price takers at a given nominal wage W. Looking at the first unit of output along the horizontal axis in Figure 7, the marginal revenue curve shows the revenue produced by that unit of output. The wage component is the marginal cost W MPL where MPL represents the marginal product of labour. The remainder, the difference between marginal revenue and marginal cost, is the amount of profit associated with the first unit of output. Similarly, each subsequent unit of output is associated with an amount of profit. Total profit at the equilibrium is equal to the sum of the profits associated with each unit of output up to equilibrium, and is hence equal to the area under the marginal revenue curve and above the marginal cost.

On scaling from micro to macro, Figure 7 reconciles micro analysis and macro aggregates. The area OABC is national income, the area above the marginal cost, global profits, and the residual area, aggregate wages. The distributive shares can be deduced directly as the ratio of both areas.

When aggregate demand from capitalists changes, the area of profits changes correspondingly. At the new equilibrium point, the shift of the marginal revenue curve

Figure 7 Kalecki’s 1936 diagram

is precisely such that the sum of shaded areas is just equal to aggregate profits, which corresponds, via the multiplier of capitalist autonomous expenditure, to investment and capitalists’ consumption, and what is left is made up of wages which bring about a demand for consumption goods equal to their amount. We hence see that while workers spend what they earn, capitalists earn what they spend.

It is clear from Figure 7 that any attempt to explain the observed cyclical behaviour of distributive shares requires us to question the determinants of the shape of the cost functions, as well as the evolution of the degree of competition. Under monopolistic competition - Kalecki (1939) coined the term “pure imperfect competition” - the micro demand curves are a family of equations yi = (P) where yi is the micro quantity, pi the individual demand price, P the general price level, ε the elasticity of demand, Y the aggregate demand, and m the number of firms present in the economy. Any change in aggregate demand entailing iso-elastic shifts in the marginal revenue curve along with increasing marginal real costs provokes a change in income distribution in favour of profits. Thus, taking into account a given degree of competition and accepting the assumption of increasing marginal cost allows him to establish the procyclicality of the profit share.

Looking at the problem from the point of view of costs, monopolistic competition allows us to do without the classical assumption of increasing marginal real cost in the short term. In the presence of excess capacity, it is indeed possible to refer to the idea that marginal cost can be taken as approximately constant, an idea first presented by Harrod (1936) and developed by Kalecki in 1938 in a paper quoted by Keynes (1939). This is the assumption that the marginal cost and average cost coincide up to a point where the normal utilization of capacity is reached, and begins to rise afterwards.

Under the assumption of a constant degree of competition, one can move directly to a relation between pricing processes via the mark-up and demonstrate the constancy of distributive shares. With constant distributive shares, the social propensity to spend is now constant and one can obtain a model isomorphic to the Keynesian model, with a linear aggregate demand curve, which can be reproduced by the familiar 45-degree figure which served to express the core of the General Theory. At the micro level, this mechanism implies a relationship between the location of the micro demand curves and the aggregate demand curve. This was accomplished by Kalecki by assuming that a shift in aggregate demand was materialized as an income effect, entailing either rightward or leftward shifts in the micro demand curve and producing successively higher or lower micro equilibriums.

It is worth emphasizing here that a change in the degree of monopoly - and thus in income distributive shares - has no effect on the level of profits. Assume the degree of monopoly has increased. By redistributing income in disfavour of workers, global consumption falls, which entails a decrease in output. Yet as long as the capitalists’ expenditures remain unchanged, the level of profit does not change: capitalists just earn a greater part of a lower gross domestic product. Graphically, this means that individual demand curve shifts leftwards until the equilibrium is restored.

Cycles and Growth

Kalecki’s analysis was explicitly dynamic. Since net investment varies, so does total capital, which influences output, investment, and savings. Kalecki did not ignore these effects, and treated the stocks of production factors and technology as variable. Taking into account the existence of a gestation period of investment, he described cycles as a succession of temporary equilibriums parameterized by a given money wage and a given capital stock, both variables resulting from investment decisions taken in the past. The model was based on the capital stock adjustment (or “flexible accelerator”) principle: current investment equals some fraction of the gap between the desired and the actual capital. The desired stock varies directly with output (taken as a proxy for the expected demand for output that the capital is to help produce). Net investment therefore depends positively on output and inversely on the initially available stock of capital.

In his 1933 version, the dynamics of Kalecki’s models came mainly from lags. Two important distinctions were introduced: one between investment decisions and actual expenditures of investment, and another between investment orders and the deliveries of equipment. With a linear mixed difference and differential system, Kalecki first thought he could explain self-sustained cycles. Owing to remarks he received from Ragnar Frisch and Nicholas Kaldor, Kalecki later made important use of non-linearities. In 1943, he assumed investment to be of the S-shape form with much lower positive slopes at both extremes than the broad middle range of the output scale: investment being assumed to be deterred both by surplus capacity and by pessimistic expectations when activity is respectively low or high. The saving curve, on the contrary, is assumed (as long as the degree of monopoly is constant) to have a constant slope. Given the output, investment depends inversely on the capital stock. Thus there are three possible equilibria, two of which are stable while the stationary one is unstable. The result is a self-sustained cycle in the real aggregates, describing how the economy moves from a stable to an unstable to another stable equilibrium. Without any reference to random shocks and Frisch’s swinging system, Kalecki hence developed a new endogenous model in which fluctuation results from waves of optimism and pessimism and the market power of firms.

Later, admitting the dampened nature of fluctuations, Kalecki explained the constant amplitude of the cycle by referring to exogenous shocks. In 1954, and finally in 1968, he returned to a linear system and introduced important modifications which have to do with the influence of development factors such as innovations and “rentiers” savings, the long-run development of a capitalist economy being positive only if technical progress exerts a stronger influence than “rentiers” savings.

Socialism

While from the 1930s to the 1960s Kalecki was associated with the socialist movement, he always stood apart from political parties, serving mainly as a consultant on economic problems.

Kalecki thought that savings were likely to increase faster than the investment necessary to expand productive capacity proportionately to full employment. As a result, if private investment was stimulated to the level of saving at full employment, there would be a continuous fall in the degree of utilization of equipment and thus a continuous fall in the rate of profit. In order to prevent the fall in the rate of profit, the government should thus intervene by increasing its spending either on public investment or on subsidies to consumption, according to social priorities. A redistribution of income from the rich to the poor would adversely affect the propensity to save. The growing interest on the National Debt he proposed to meet from an annual capital tax or from a “modified income tax”, designed so as to offset any adverse effect of additional taxation on the propensity to invest.

Convinced that full employment policies could be secured by appropriate fiscal and budgetary policies, he did not ignore the political aspects which these policies were likely to raise. Because of financial imperfections - which are implicit in Marx’s schemes of reproduction, and to which Kalecki constantly referred - capitalists as a class have great power in the determination of the growth rate. Being alone in determining the level of investment and thus the level of activity, capitalists as a class have control over the level of employment. However, the preservation of their social position comes before the quest for profit. This is why, because government interventions are likely to weaken their political influence by achieving full employment and thus increasing the workers’ bargaining power, the capitalist may accept a higher rate of unemployment in order to restore “the discipline in the factories”, even if this comes with a lower rate of profit. It is thus only by profound institutional changes that the class conflicts can be overcome, but, in that case, the economy will be more socialist than capitalist.

Michael Assous

See also:

Business cycles and growth (III); Roy Forbes Harrod (I); Keynesianism (II); Marxism(s) (II); PostKeynesianism (II).

References and further reading

Assous, M. (2007), ‘Kalecki’s 1934 model vs. the IS-LM model of Hicks (1937) and of Modigliani (1944)’, European Journal of the History of Economic Thought, 14 (1), 97-118.

Chamberlin, E. (1933), Theory of Monopolistic Competition, Cambridge, MA: Harvard University Press.

Chapple, S. (1995), ‘The Kaleckian origins of the Keynesian model’, Oxford Economic Papers, 47 (2), 525-37.

Feiwel, G.R. (1975), Michal Kalecki. A Study in Economic Theory and Policy, Knoxville, TN: University of Tennessee Press.

Harrod, R.-F. (1936), The Trade Cycle. An Essay, Oxford: Clarendon Press.

Hicks, J. (1937), ‘Mr. Keynes and the “Classics”: a suggested interpretation’, Econometrica, 5 (2), 147-59.

Kalecki, M. (1934), ‘Trzy uklady’, Ekonomista, 34, 54-70, English trans. ‘Three systems’, in J. Osiatynski (ed.) (1990), Collected Works of Michal Kalecki, vol. 1, Capitalism, Business Cycles and Full Employment, Oxford: Clarendon Press, pp. 201-19.

Kalecki, M. (1936), ‘Pare uwag o teorii Keynesa’, Ekhonomista, 36, 18-26, English trans. ‘Some remarks on Keynes’s theory’, in J. Osiatynski (ed.) (1990), Collected Works of Michal Kalecki, vol. 1, Capitalism, Business Cycles and Full Employment, Oxford: Clarendon Press, pp. 223-32.

Kalecki, M. (1938), ‘The determinants of the distribution of national income’, Econometrica, 6 (2), 97-112.

Kalecki, M. (1939), ‘The supply curve of an industry under imperfect competition’, Review of Economic Studies, 7 (2), 91-112.

Kalecki, M. (1944), ‘Prof. Pigou on “the classical stationary state”. A comment’, Economic Journal, 54 (2), 131-2.

Kalecki, M. (1990), Collected Works of Michal Kalecki, vol. 1, Capitalism, Business Cycles and Full Employment, J. Osiatynski (ed.), Oxford: Clarendon Press.

Keynes, J.M. (1936), The General Theory of Employment, Interest and Money, London: Macmillan.

Keynes, J.M. (1939), ‘Relative movements of real wages and output’, Economic Journal, 49 (March), 34-51.

Leijonhuvfud, A. (1968), On Keynesian Economics and the Economics of Keynes, New York: Oxford University Press.

Lopez, J. and M. Assous (2010), Michal Kalecki: An Intellectual Biography, Basingstoke: Palgrave Macmillan. Marx, K. (1976), Capital, Volume I, trans. B. Fowkes, Harmondsworth: Penguin.

Modigliani, F. (1944), ‘Liquidity preference and the theory of interest and money’, Econometrica, 12 (1), 44 88.

Robinson, J. (1966), ‘Kalecki and Keynes’, in P.A. Baran (ed.), Problems of Economic Dynamics and Planning: Essays in Honour of Michal Kalecki, London: Pergamon Press.

Tobin, J. (1975), ‘Keynesian models of recession and depression’, American Economic Review, 65 (2), 195-202. Toporowski, J. (2013), Michal Kalecki: An Intellectual Biography, vol. 1, Rendez-vous in Cambridge 1899-1939, New York: St Martin’s Press, Palgrave Macmillan.