Maurice Allais was born in Paris on 31 May 1911 and died in Saint-Cloud on 9 October 2010.

He was admitted to the Ecole Polytechnique in 1931, studied also at the Ecole des Mines from 1934 to 1936 and then started to work in Nantes as an engineer. But since his time as a student, his interests had changed.

His first interests were in theoretical physics - he was to come back to this subject at the end of his life - but he turned to economics. In 30 months, from January 1941 to July 1943, he wrote his Traite d’economiepure. This work was intended to be the first of eight volumes, a series entitled A la recherche d’une discipline economique, supposedly to deal successively with pure economics, real economy and the economy of the future. He gave up his ambitious project but it is possible to find in Economie et interet, published in 1947, part of the material he had prepared for his magnum opus, that is, the areas which dealt with interest, money and disequilibria affecting the real economy.In 1946 Allais became a senior research fellow at the Centre National de la Recherche Scientifique. He also lectured at the Paris Ecole des Mines (1944-88), at the Institut de Statistiques of the University of Paris (1947-68) and at the University of Paris X Nanterre (1970-85). He was awarded the 1988 Sveriges Riksbank’s Prize in Economic Sciences in Memory of Alfred Nobel for his contribution to the theory of markets and efficient use of resources, with the nominating committee explicitly referring to Traite d’economie pure and Economie et interet. It stressed that “Allais’ distinguished contribution may to some extent be regarded as a parallel to two important works published around the same time... : Value and Capital (1939) by Sir John Hicks and Foundations of Economic Analysis by Paul A. Samuelson (1947)” (in Allais 1989: 2).

Allais (1989: 5) affirmed that his subsequent works are only developments and complements to the Traite.

However his discourse evolved. In 1943, he maintained that the complexity of the problems was such that they could only be analysed with mathematics. In the 1950s, he was more cautious. The problem lies in the fact that “in a science like economics, the rigour of the mathematical deductions can be deceptive. What matters is only the discussion of the premises and the results” (Allais 1954: 68).The Traite is an important step in the renewal of general equilibrium models. But, at the end of the 1960s, Allais also developed a radical critique of such models and proposed a dynamic approach based on the search of obtainable surpluses. And while his first publications deal with pure economics, at the end of his life he devoted more time to empirical works and to questions of economic policy.

The Theory of Equilibrium

Allais dedicated his Traite to Leon Walras, Vilfredo Pareto, Irving Fisher and Franςois Divisia. He wanted to make a synthesis and go farther. He thought that their theories were essentially static and his ambition was to introduce time in order to obtain a dynamics of equilibrium. In such a model, the choices of the agents depend on actual and future prices. However, at this stage Allais wanted to eliminate risk; he thus supposed that “any decision taken now and implying the future is verified” (1943 [1994, 3rd edition]: 60). This hypothesis led him to think that there exist as many elementary markets as future goods and services.

When, in the first parts of Elements d’economiepolitique pure (Walras 1874-77 [1988]), Walras studies an economy deprived of circulating money, he does not explain how exchanges and payments are made. Allais (1943 [1994, 3rd edition]: 536) is more explicit. He deals with an “economie de compte”, different from a barter economy. Prices are expressed in a money detached from all material connotation. Exchanges are centralized; a clearing house counts the revenues and expenses of the agents and settles the accounts through transfers.

Allais thus defines the framework of the majority of general equilibrium models. He did not pose the questions of the existence and uniqueness of equilibrium. The problem that interests him is stability. In an exchange economy, he supposes that the utility functions of the agents are separable. The process of adjustment depends on four restrictive hypotheses, typical of the Walrasian model: (1) the price system is unique, whether the system in equilibrium or not; (2) if in a market supply exceeds (falls short of) demand, the price diminishes (increases); (3) prices do not simultaneously adjust in all markets, but successively; and (4) exchanges are only made at equilibrium prices. To study convergence, Allais introduces a characteristic function defined as the sum of the absolute values of the differences between the values of supplies and demands:

If, for all individuals, the value of demand of a good varies inversely to its price, the value of the characteristic function diminishes when its price adjusts, and equilibrium is stable. If this is not the case, but if, in the neighbourhood of equilibrium, the value of the global demand of a good increases less rapidly than the value of the global supply when the price rises, equilibrium is stable (Allais 1943 [1994, 3rd edition]: 477). Negishi (1962: 656) showed that Allais’s hypotheses boils down to the assumption that goods are gross substitutes; if the price of a commodity rises while all other prices are unchanged, the demand for the other commodities increases.

Surplus, Social Return and Dynamics of the System

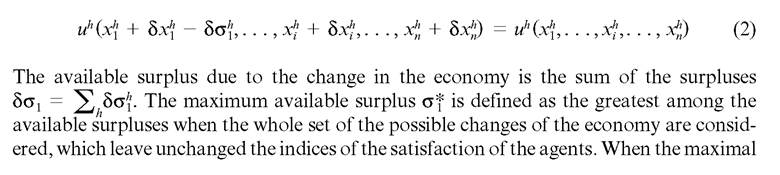

Pareto had rejected the Marshallian notion of surplus. But, in his Manuele (1906: 655-6), he proposed a new, somewhat sibylline, definition of it. Allais - who became aware of the work of Dupuit in 1973 only and thought very high of it - picked it up. Let h be an individual who, in the initial situation, has a quantity xhi of good i.

Suppose that, in a new situation, it has a quantity xhi + dhi thereof. Allais measures the surplus from which this individual benefits in the new situation with the quantity δσh of good 1 which, if it were withdrawn from it, would bring back the individual’s satisfaction to the level it was in the initial situation:

available surplus is nil, it is impossible to improve the situation of a person without worsening that of another person, and the efficiency of the economy is at a maximum.

Allais then states, in 1943, the two propositions of what he calls the “Theoreme du rendement social” - later known as the two theorems of welfare economics - (1) any situation of maximum efficiency is a market equilibrium, and (2) any market equilibrium is a situation of maximum efficiency. In Economie et interet, he generalizes the notion of social return to take future generations into account. The social return is said to be at maximum when any change of the state considered, which increases the satisfaction of some individuals in certain periods, diminishes the satisfaction of the same or other individuals but in some other periods.

What are the consequences of these propositions? Allais discards at the same time planning and laissez-faire. The maximization of the social return, he stresses, cannot be realized in laissez-faire conditions. In industries with increasing returns, monopolies will prevail and, fixing a price greater than the marginal cost, prevents the realization of the optimum. In the other activities, the imperfection of competition - and particularly the absence of markets for future goods - leads to a suboptimal allocation of resources. Against planning, Allais stresses that the determination of prices is a central question, which can only be solved by markets. To deprive oneself of this mechanism means to forbid any rigorous economic calculation.

However, the necessity to resort to markets leaves the question of the property of the means of production completely open.The economic organization must rely on autonomous economic agents, having, each according to its share, the free disposal of the economic goods... But one can imagine a society... in which the various company managerial staffs could have... this free disposal... without the ownership of the means of production ceasing to be collective. (Allais 1943 [1994]: 663)

At that time many French companies were nationalized and Allais thought that the system could work smoothly provided that the managing staffs of the public firms had an effective power of decision.

Neo-Walrasian models of general equilibrium deal with an economy, in which agents’ supply and demand goods in a centralized market in function of a general and centralized system of prices, which is announced to them. Allais (1971: 369; 1981 [1989]: 359) proposes instead a model of a decentralized search for surplus. He imagines an economy, where each agent is looking for one or more partners, who would accept an exchange susceptible to generate a surplus to be shared. Equilibrium is thus defined as the situation where there is no possibility to generate a surplus. It is an optimum. While, in a Walrasian economy, exchanges are made at the same time, at equilibrium prices determined by the tatonnememt, Allais describes the path to equilibrium, which results from successive exchanges made at different prices.

Choices under Uncertainty

In Traite, Allais abstracted from uncertainty, but he studied the question in 1953 when he discussed the analyses made at that time of the behaviour of a rational man facing risk. Bernoulli’s idea that the agents maximize the mathematical expectation of their utility had been picked up and transformed (Friedman and Savage, 1948). An ordinal index of preferences had been substituted for the measure of cardinal utility and it was admitted that the probabilities taken into account in choices were subjective and not objective.

To formalize the behaviour of a rational agent, Paul Samuelson (1952) had introduced an independence axiom. Suppose that an individual prefers lottery p to lottery q. Let r be some other lottery, and a a probability. The independence axiom states that:

This implies that if two lotteries have a common part (1 - α)r, the preference order is not modified by a change in this part. To show that this axiom is not self-evident, Allais proposed the following experiment. One first asks a person whether he or she prefers to receive 100 million euro (situation A) - the size of the sum is crucial in the experiment - or to participate in a lottery where there is a 10 per cent probability of winning 500 million, 89 per cent of winning 100 million and 1 per cent of not winning anything (situation B). Then this person is asked whether he or she prefers to receive 100 million with a probability of 11 per cent and nothing with a probability of 89 per cent (situation C) or to receive 500 million with a 10 per cent probability and nothing with a probability of 90 per cent (situation D). The independence axiom implies that the individual who prefers C to D will prefer A to B, and conversely: when shifting from C to A or from D to B, only the common part is modified, which, with a probability a equal to 89 per cent, allows a gain of 100 million in lotteries A and B, and nothing in lotteries C and D. However, many persons among those who took part in the test, preferred D to C while preferring A to B. This result is often presented as a paradox - Allais’s paradox. But Allais stresses that this is no paradox and that the problem with the theory of the expected utility is that it neglects the dispersion of the gains. When important sums of money are at stake, many choose security in the neighbourhood of certainty, and this explains that they prefer A to B, that is, the certainty to have 100 million rather than to participate in a lottery where they could win 500 million but also lose everything. The expected utility theory does not only lack an empirical foundation, it is also based on an arbitrary definition of rationality.

Money and Cycles

In Economie and interet, Allais tries to explain why the economic agents prefer to keep money rather than buy assets likely to bring them an interest. He thinks that “the reason why economic agents have cash balances is the existence of costs for... the negotiation of assets or the realization of investments or bonds according to their needs” (Allais 1947

bonds according to their needs” (Allais 1947

In an appendix to this book Allais develops a scheme to analyse the factors, which determine the interest rate. The economy is supposed to entail a single category of agents, whose life consists of two periods of equal duration. During each period, two generations of agents coexist: the younger and the elder. Each individual works only during his

youth, and there is no inheritance. Money is introduced as a means of payment and store of value. Owing to the non-synchronization of incomes and expenses, the young agents need a cash balance, which will allow them to buy consumption goods during their old age. In this context, Allais establishes a series of results:

1. The use of a medium of circulation increases the interest rate above the level it would have in an account economy because holding money satisfies in part the propensity to save and thus slows the accumulation of real capital.

2. The equilibrium interest rate is an increasing function of the preference for the liquidity, but does not depend on the quantity of money.

3. The depreciation of money diminishes the values of the interest rate, which correspond to stable equilibria.

In 1953, Allais developed a monetary theory of the business cycle. For him, “there are only two ‘sine qua non’ factors for the cycle: the fact that the circulating medium can be hoarded, and the possible issuing of overdraft money” (Allais 1953b [2001]: 228). The model has four central equations. (1) During a period, the global expense is equal to the revenue of the previous period plus the excess of the actual over the desired cash balances. (2) The ratio of the total desired cash balance on the total expense is a decreasing function of the rate of growth of the total expense: agents diminish their balances during expansion and increase them during recessions. It is the classical phenomenon of hoarding. (3) The global quantity of circulating medium (notes plus deposits) is an increasing function of the rate of growth of the total expense: during expansions, commercial banks lower their rate of reserves and they increase it during recessions. (4) Finally, in each period, expense equals income. Under very general hypotheses, there is no stable equilibrium and, from any state of the system, the economy tends to a limit cycle.

In this context, Allais (1965 [2001]) proposed a new version of the quantity theory of money, based on a restatement of the function of demand for money - hereditary, relative and logistic. The demand for money is hereditary in the sense that the relative demand for money - defined as the ratio of the desired cash balance on the expense - is a function of the past evolution of the global expense; it is relative because the rate of oversight is not a constant but depends on the business cycle: the past is forgotten even more rapidly as the historical context was troubled; it is logistic because the relative demand for money is a logistic function of a coefficient of psychological expansion. Allais thus shifted from an essentially theoretical approach in the 1940s to another approach, which puts emphasis on the statistical analysis of empirical data.

Alain Beraud

See also:

John Richard Hicks (I); Vilfredo Pareto (I); Paul Anthony Samuelson (I); Marie-Esprit-Leon Walras (I).

References and further reading

Allais, M. (1943), A la recherche d’une discipline economique, premiere partie, L’economie pure, vol. 1, Paris: Chez l’auteur, 2nd edn 1952 as Traite d’economie pure, Paris: Imprimerie nationale, 3rd edn 1994, Paris: Clement Juglar.

Allais, M. (1947), Economie et interet, Paris: Imprimerie nationale, 2nd edn 1998, Paris: Clement Juglar.

Allais, M. (1953a), ‘Le comportement de l,homme rationnel devant le risque: critique des postulats et axiomes de l’ecole americaine’, Econometrica, 21 (4), 503-46.

Allais, M. (1953b), ‘Illustration de la theorie des cycles economique dans un modele monetaire non lineaire’, Communication au Congres Europeen de la Societe d’Econometrie, reproduced in M. Allais (2001), Fondements de la dynamique monetaire, Paris: Clement Juglar.

Allais, M. (1954), ‘Puissance et dangers de l’utilisation de l’outil mathematique en Economique’, Econometrica, 22 (1), 58-71.

Allais, M. (1965), Reformulation de la theorie quantitative de la monnaie, Paris: SEDEIS, reproduced in M. Allais (2001), Fondements de la dynamique monetaire, Paris: Clement Juglar.

Allais, M. (1971), ‘Les theories de l’equilibre economique general et de l’efficacite maximale. Impasses recentes et nouvelles perspectives’, Revue d’economiepolitique, 81 (3), 331-409.

Allais, M. (1981), ‘La theorie generale des surplus’, Economies et Societes, serie Economie Mathematique et Econometrie, 8 and 9, new edn 1989, Grenoble: Presses Universitaires de Grenoble.

Allais, M. (1989), ‘Les lignes directrices de mon (Friedman and Schwartz 1963).

One of the recurring themes in Friedman’s scientific, journalistic and political work was freedom in the form of a market society without governmental interference. He promoted capitalism as a necessary (yet not sufficient) condition for political freedom not only in the United States but also abroad, including non-democratic countries. One of his journeys took him to Chile in 1975 where he advised Augusto Pinochet to act against inflation and take back the recent nationalizations of important businesses. Critics blamed him for aiding a dictatorship, but Friedman always characterized himself as a mere expert and added that dictatorial regimes were more likely to convert to democracies than totalitarian communist societies (among which he counted the regime of Pinochet’s predecessor Salvador Allende).

The presentation of the Sveriges Riksbank Prize in Economic Sciences to Friedman in 1976 was overshadowed by protests against him. He then retreated from the University of Chicago and took a position at the Hoover Institution on War, Revolution and Peace at Stanford University in California and stayed there until his death in November 2006.

Work

Friedman was awarded the Sveriges Riksbank Prize “for his achievements in the fields of consumption analysis, monetary history and theory, and for his demonstration of the complexity of stabilization policy”. Not mentioned was what might be called his decadelong crusade for a “pure” market economy, which he saw endangered by a well-meaning welfare and tax state. See his essays on the abolishment of the military draft as well as the mail monopoly, on the privatization of social security, the legalization of drugs, or the promotion of private schools (Friedman 1962).

Consumption theory

Chronologically, consumption analysis was Friedman’s first important field of interest. In the beginning, he approached the area empirically, working on The Study of Consumer Purchases for the National Resources Committee in Washington, DC (United States Resource Committee 2009) and, after Simon Kuznets invited him to work at the NBER in 1937, on the income of freelancers. Part of the resulting Income from Independent Professional Practitioners (Friedman and Kuznets 1954) also formed his dissertation at Columbia; however, publication was delayed from 1941 until 1945 by intense discussions of certain implications it held, namely that the regulation of entry into medicine increased its price and impaired its supply.

His first major work, A Theory of the Consumption Function, was published in 1957. From a theoretical point of view, it marked a counterpoint to the then common mathematic representation of consumption used in Keynesian macroeconomics, which saw households’ expenditures proportional to current income and seemed somewhat mechanistic and unfounded. Friedman instead described the consumption level as a function of “permanent income”: rational households discount their real wealth with the interest rate in order to yield an estimate of future, or lifetime, income. Even though empirical economics by and large kept using the Keynesian concept, Friedman managed to introduce the fundamentally different perspective of an intertemporally optimizing individual agent (as opposed to the conventional household routine of consuming a certain proportion of every increase in income).

Thus he provided “microeconomic foundations” to consumption as a macroeconomic aggregate. In this respect, Friedman built on Irving Fisher whose time preference theory had already linked optimal distribution of consumption over several periods to interest rates - from which Keynes had deviated deliberately.

A disagreement about assumptions concerned the inherent stability of the economy, leading to full employment through market forces, which Friedman always claimed, but never established. This is directly connected to consumption because if economic agents are hindered in employing their abilities (their wealth) in the markets - for example, by involuntary unemployment - they are forced to adjust expenditures in the short term, that is, regardless of their longer-term permanent income. Nonetheless, the abolishment of a constant propensity to consume puts in doubt the existence of a (government expenditures) multiplier effect since households are not thought to react proportionally to current-income increases anymore, thus potentially making demand management less effective.

Further discussion revolved around an implicit assumption stemming from the divergence of current and permanent income: in order to maintain an even consumption level over time, agents need to be able to obtain credit and invest money without restrictions on perfect financial markets. However, concepts like risk aversion, information asymmetry and reputational deficits render this assumption invalid. Expected income and human capital are not (or only to a very small extent) eligible as collateral in credit contracts so that households in fact have to rely on their current instead of their permanent income. Furthermore, modern micro theory found more arguments in favour of the Keynesian consumption function by integrating norms into the utility function (Akerlof 2007).

Money demand

Friedman entered into a constructive dispute with Keynesianism by reviving the quantity theory of money. At its heart is the quantity equation MV ? PY which describes the tautological relationship of the nominal transaction value, that is, (real national product Y times price level P), and its “technical” funding by an amount of money M that circulates through the economy with a certain velocity V (Fisher had used the sum of nominal transactions instead of nominal income). The quantity theory states that if velocity is stable and real aggregate output cannot be influenced by monetary policy, prices move along with the amount of money.

The velocity of money is the inverse of agents’ propensity to hold real balances, that is, money demand; the approach thus builds on the traditional Cambridge k. In 1956, Friedman published a “Restatement” of money demand theory and explained the difference from the old quantity theory as follows: “For the transactions version [of the

quantity theory], the most important thing about money is that it is transferred. For the income version, the most important thing is that it is held” (Friedman 1974: 8). Money demand is seen as an element of portfolio selection concerning a wide range of assets, and depends on income and on the vector of market returns.

Friedman’s restatement made two important contributions. First, it made clear that transmission of interest rate changes not only runs from net investment to consumption: since securities and long-lived consumption goods are substitutes, a change in asset prices induced by interest rate policy can affect goods demand directly. Thus, the often unpredictable investment reaction as a potential weak spot in monetary macroeconomic stabilization can be circumvented. Second, and in contrast to classical economics, the velocity of money V is no longer constant but a stable function of other macroeconomic variables.

According to Keynes (1936: 164), a monetary expansion (rising M) can seep away in the “liquidity trap” (which implies a decreasing V). In this case, economic activity cannot be influenced by monetary policy anymore. During the world economic crisis of the 1930s, both production and prices fell. However, Friedman ascribed this to a significant decrease in the amount of money instead of an unstable velocity: because the Federal Reserve, in a blend of ignorance and misconceived competition policy, had let several struggling banks fail, broad money was diminished and chains of payment disrupted, leading to income and wealth decreases, bank runs, and hoarding of money. In his eyes, the crisis was just proof not of the market system’s instability (as many Keynesians saw it) but of the incompetence of economic policy. His conclusion was that “money is much too serious a matter to be left to the Central Bankers” (Friedman 1962: 51). Ever since, he demanded a limit to central bank autonomy and money to be subject to a fixed percentage growth, which he deemed sufficient for growth, full employment, and price stability.

Monetary policy

As president of the American Economic Association, Friedman worked on the stabilizing “Role of monetary policy” (1968) more intensively, building on the negative relationship between inflation and unemployment as described by the Phillips curve which was discovered empirically only a few years earlier. Against this background, there was a discussion about the idea that economic policymakers could possibly choose any point on the curve, that is, for example, lower unemployment at the cost of accepting a higher rate of inflation. Friedman now analysed such a monetary expansion, assuming a “natural rate” of unemployment which is not cyclical but structural, that is, caused by inefficient markets and social structures such as insufficient workforce mobility. In this situation in which employment is at its short-term maximum, excess demand on labour markets leads to wage and price increases, with inflation expectations becoming increasingly important for wage demands. Hence, an additional motive (apart from and independent of the level of employment) enters the determination of wage and price growth rates - the Phillips curve is therefore only valid for given inflation expectations and moves up if they increase, resulting in higher inflation for any given rate of unemployment.

A monetary expansion can increase employment temporarily at most, namely, if nominal-wage growth stays below the actual rate of inflation. In the long run, there is no choice between inflation and unemployment, but only between low and high inflation at a given “natural rate” of unemployment that can be moved by supply-side measures (for example, aimed at flexibility, education, and productivity). This core message - demand-side policies cannot push the economy beyond full-employment for long - is considered trivial today and had already been advanced earlier by Keynes (1936: 289). Still, it received a lot of attention at the time and was fought heavily in the 1960s, especially by Keynesians.

Several explanations are conceivable. First, the “natural rate” is not a clear-cut point estimate, making it desirable for policymakers to “try” the supply restrictions imposed by the labour market. However, Friedman abstracts from such a lack of information in his model. Second, as Tobin (1972: 17) had already mentioned, cyclical underemployment can become structural. Under certain conditions, this process can also be reversed, that is temporary over-employment could lower the “natural rate” by re-qualifying formerly structurally unemployed in the production process and thus increasing the marketable labour force potential. However, this argument was developed only in the “hysteresis” debate in the 1980s (Jenkinson 1987). Third, Keynesians in the 1960s were so used to the assumption of unemployment that they overlooked Friedman’s starting point - full employment - and subsequently engaged in a pointless argument. “Keynesians were concerned with the problem of pushing the economy to its natural rate, not beyond it. If the economy is already there, we can all go home” (Hahn 1982: 74-5) - Friedman merely added that unemployment rates below the “natural level” cannot be sustained.

Based on his work, the monetarist economic school of thought developed - the term “monetarism” goes back to Brunner (1968) - which considers the amount of money as the driving force of economic activity. In contrast to his monetarist peers, however, Friedman preferred simple models and clear messages, for example, his famous “helicopter money” parabola (Friedman 1969). This is in accordance with his position on methodology (Friedman 1953a): from his point of view, economic science is not about the realism of assumptions but instead about empirical validity of hypotheses, in this specific case a predictable relationship between money and prices. However, Friedman’s use of theories was rather eclectic, using ad hoc either Walras’s or Marshall’s equilibrium theory, or even the Keynesian IS-LM model. This produced an open debate about his “Theoretical framework for monetary analysis” (1974) and led Hahn (1971: 62) to criticize his “lack of seriousness”.

Impact

How are Friedman’s scientific works and his economic policy advice to be assessed? The academic profession displays an ambiguity in this respect that is surprising for a world- renowned Sveriges Riksbank Prize laureate. Krugman (2007) attributed to Friedman three different personalities: while he is said to have attracted universal admiration as an economist, his other two personae - as a “policy entrepreneur” advocating monetarism and an ideologue demanding liberalization and deregulation in many respects - were met with stronger opposition. Krugman even calls Friedman “intellectually dishonest” in defending his views on policy. A closer look at Friedman as a person as well as his works reveals a consistency in his beliefs, publications and activities. Clear speech, the inclination to taper and simplify whenever possible, but also often describing problems only monocausally, explain his success in transferring his arguments from theory into practice.

The invisible hand of competition and the macroeconomic power of the amount of money are recurring motives while governing the economy is always criticized fiercely: “benevolent dictatorship is likely sooner or later to lead to a totalitarian society” (Friedman 1997: 22). At the centre of his economic concept stands ultimately a homo oeconomicus who is Free to Choose (which is the title of a television series aired in the 1980s, and also of a book jointly written with his wife Rose - Friedman and Friedman 1980). Friedman thus counts among the pioneers of the microfoundation of macroeconomics. However, he did not follow what was made of this by fellow economists afterwards: in combination with rational expectations, and pushing his Phillips curve analysis ever further, they arrived at new classical macroeconomics or, as Tobin (1980) called it, “Monetarism Mark II”, in which rational agents know about the long-term effects of a monetary expansion and therefore only adjust prices but no real variables even in the short run. By contrast, Friedman always opposed such model-driven implications and emphasized the short- and medium-term non-neutrality of monetary policy on growth and employment. However, he did so not to steer central banks’ attention towards day-to-day business but, rather, to indicate the economic costs of monetary policy when targeting the short term.

The transition towards money supply control was without doubt Friedman’s greatest achievement with respect to (monetary) policy. In the mid-1970s, central banks in Germany and Switzerland, later also in England and the United States, implemented a monetary strategy that, at least at first sight, conformed to his demand for a slow, rulebased expansion of money supply. The “monetarist counter-revolution” put price stability before employment again, which also required central banks to be independent of foreign exchange markets, that is, required a system of flexible exchange rates (Friedman 1953b); however, Friedman like many economists did not anticipate the at times very strong exchange rate movements after the collapse of the Bretton Woods system. In 1975, the German Bundesbank was the first central bank to introduce money supply control, and its success in keeping inflation in check added greatly to the reputation of Friedman’s ideas.

On a closer look, however, neither the Bundesbank nor other central banks actually followed Friedman’s guideline of an optimal money growth. Instead, they practised interest rate policy and used the monetary target (which was missed about half of the time) merely as a means of “public relations”. Since the European Central Bank has become Europe’s first monetary authority, the role of money supply as an intermediate policy goal was diminished even further.

Having had very little success in predicting inflation rates using the quantity theory in the 1980s, Friedman became more flexible towards the end of his life. In his latest scientific work (2005) he shifted focus from goods to asset price inflation. He also predicted in a German newspaper severe political and economic tensions that might well lead to the breakdown of a future European Monetary Union.

Christian Philipp Schroder and Peter Spahn

See also:

Chicago School (II); Monetarism (II); Money and banking (III).

References and further reading

Akerlof, G.A. (2007), ‘The missing motivation in macroeconomics’, American Economic Review, 97 (1), 5-36.

Brunner, K. (1968), ‘The role of money and monetary policy’, Review, Federal Reserve Bank of St Louis, 9-24.

Ebenstein, L. (2007), Milton Friedman. A Biography, London: Palgrave Macmillan.

Friedman, M. (1953a), ‘The methodology of positive economics’, in M. Friedman, Essays in Positive Economics, Chicago, IL: Chicago University Press, pp. 3-43.

Friedman, M. (1953b), ‘The case for flexible exchange rates’, in M. Friedman, Essays in Positive Economics, Chicago, IL: Chicago University Press, pp. 157-203.

Friedman, M. (1956), ‘The quantity theory of money: a restatement’, in M. Friedman (ed.), Studies in the Quantity Theory of Money, Chicago, IL: Chicago University Press, pp. 3-21.

Friedman, M. (1957), A Theory of the Consumption Function, Princeton, NJ: Princeton University Press.

Friedman, M. (1962), Capitalism and Freedom, Chicago, IL: Chicago University Press.

Friedman, M. (1968), ‘The role of monetary policy’, American Economic Review, 58 (1), 1-17.

Friedman, M. (1969), ‘The optimum quantity of money’, in M. Friedman, The Optimum Quantity of Money and Other Essays, Chicago, IL: Aldine, pp. 1-50.

Friedman, M. (1974), ‘A theoretical framework for monetary analysis’, in R.J. Gordon (ed.), Milton Friedman’s Monetary Framework - A Debate with His Critics, Chicago, IL: Chicago University Press, pp. 1-62.

Friedman, M. (1997), ‘John Maynard Keynes’, Economic Quarterly, 83 (2), Federal Reserve Bank of Richmond, 1-23.

Friedman, M. (2005), ‘A natural experiment in monetary policy covering three episodes of growth and decline in the economy and the stock market’, Journal of Economic Perspectives, 19 (4), 145-50.

Friedman, M. and R. Friedman (1980), Free to Choose: A Personal Statement, New York: Harcourt.

Friedman, M. and S. Kuznets (1954), Income from Independent Professional Practice, Cambridge, MA: National Bureau of Economic Research.

Friedman, M. and A.J. Schwartz (1963), A Monetary History of the United States, 1867-1960, Princeton, NJ: Princeton University Press.

Hahn, F.H. (1971), ‘Professor Friedman’s views on money’, Economica, 38 (149), 61-80.

Hahn, F.H. (1982), Money and Inflation, Oxford: Blackwell.

Jenkinson, T. (1987), ‘The natural rate of unemployment: does it exist?’, Oxford Review of Economic Policy, 3 (3), 20-26.

Keynes, J.M. (1936), The General Theory of Employment, Interest and Money, London: Macmillan.

Krugman, P. (2007), ‘Who was Milton Friedman?’, New York Review of Books, 54 (2), 27-30.

Tobin, J. (1972), ‘Inflation and unemployment’, American Economic Review, 62 (1/2), 1-18.

Tobin, J. (1980), Asset Accumulation and Economic Activity, Oxford: Basil Blackwell.

United States National Resources Committee (2009), Study of Consumer Purchases in the United States, 1935-1936, Ann Arbor, MI: Inter-university Consortium for Political and Social Research.