Endogenous Irregular Fluctuations

We have already noted that probably the vast majority of economists do not accept that macroeconomic fluctuations exhibit definite periodicities of any length, including many of those who accept that such fluctuations are substantially endogenous in character, with only a few of those stressing exogenous sources seeing any possibility of this, notably Jevons (1878) who saw sunspots as the periodic exogenous driver.

However, gradually many came to realize that if crucial relationships, particularly those involving capital investment, are nonlinear, then endogenous fluctuations can arise that may be not only periodically regular, but aperiodically erratic in a variety of ways. Venkatachalam and Velupillai (2012) argue that the first to realize this possibility was Hamburger (1930), who was inspired by the physics models of relaxation oscillations of van der Pol (1926), drawing on the earlier work of Poincare (1908).Hamburger was followed by Le Corbeiller (1933), who in turn personally influenced the crucial work of Goodwin (1951) whose nonlinear accelerator model was shown by Strotz et al. (1953) to be capable of generating endogenous erratic fluctuations that could possibly be chaotic. However, probably the first to develop a model capable of generating chaotic dynamics was Palander (1935) whose regional dynamics model exhibited three-period cycles, shown by Sharkovsky (1964) and Li and Yorke (1975) to be sufficient in one-dimensional models to produce chaotic dynamics. While none of these realized at the time what they had shown, Goodwin (1990) would later become a committed student of endogenous chaotic dynamics in nonlinear economic models. Chaotic dynamics exhibit sensitive dependence on initial conditions, known popularly as the “butterfly effect”, in which small changes in a control parameter or a starting point can lead to large changes in the dynamic pattern (Rosser 2000: ch.

2).Independently, various economists associated with Keynesian economics developed models with nonlinearities that they realized could endogenously generate periodic cycles (Kalecki 1935; Kaldor 1940; Metzler 1941; Hicks 1950), with later economists understanding that these models could generate various forms of complex aperiodic dynamics. Variations on the Kaldor model, particularly by Chang and Smyth (1971) have been shown to exhibit a wide variety of complex dynamics, including catastrophic discontinuities (Varian 1979; Rosser 2007). Zeeman (1974) applied this to stock market crashes (drawing on Thom 1972), chaotic dynamics (Dana and Malgrange 1984), and

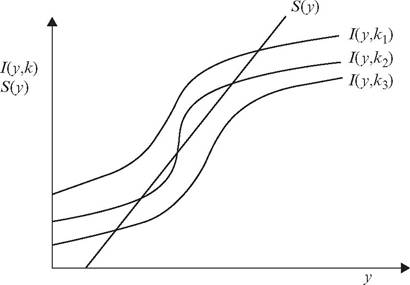

Figure 2 Shifting Kaldorian nonlinear investment functions

transient chaos as well as fractal basin boundaries with multiple attractors (Lorenz 1992). Key to the Kaldor model dynamics is a nonlinear sigmoid function relating output with investment, with this investment function shifting over the course of a business cycle as the capital stock varies. As the investment function shifts, discontinuous changes in investment happen. This is depicted in Figure 2.

Full recognition of how wide the conditions are under which deterministic chaotic dynamics can happen only came about in the 1980s (Rosser 2000). Among the first to be explicitly studied in this way were overlapping generations models (OLG) that followed the formulation of Gale (1973). Benhabib and Day (1980) showed that a sufficient degree of substitutability in the intergenerational offer curves can lead to endogenous chaotic dynamics, although presumably these would be fluctuations more along Kuznetsian long-swing time periods rather than shorter-term fluctuations. Grandmont (1985) extended this, bringing in risk aversion and interest rates (and thus implicitly potentially monetary policy) to show that chaotic dynamics can arise if older agents have a sufficiently higher marginal propensity to consume leisure than younger agents.

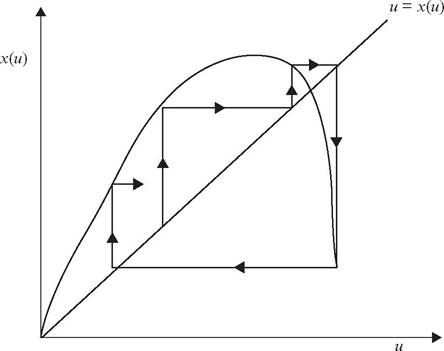

Keeping in mind that in one-dimensional systems a three-period cycle is a sufficient condition for the existence of chaotic dynamics, Figure 3 depicts such a cycle where μ represents real balances today and x(μ) real balances tomorrow.Chaotic dynamics have been shown to be possible in neoclassical models of agents with multiple sectors and infinitely lived agents, hence not just OLG models where things can happen (such as rational speculative bubbles) that do not in representative agent models. Day (1982) provides one such example that involves an upper limit on the capital-labour ratio, suggested by him to be due to a pollution limit. This leads to a standard Solow growth model turning into one with a logistic function determining the dynamics of the sort shown to exhibit chaotic dynamics by Robert May (1976). This model by Day can serve as a driver for a model of much greater financial volatility through the mechanism of “flare attractors” (Rosser et al. 2003) as first posed by Rossler and Harmann (1995).

Another take on this without any “ad hoc” variation from the neoclassical approach is to find that with a sufficiently high discount rate, “every possible” sort of behaviour can happen in a conventional growth model (Boldrin and Montrucchio 1986; Mitra 1996;

Figure 3 Chaotic Grandmont monetary dynamics

Nishimura and Yano 1996). We note that these models all assume full optimization as well as perfect knowledge by an infinitely lived agent. However, generally the discount rates at which chaos appear are very high, although lower as the number of factors of production increases.

Returning to the world of more post-Keynesian models without representative infinitely lived fully informed and rational agents, more complex dynamics have been observed in other variations of models. Goodwin (1967) proposed a model of endogenous regular business cycles driven by class struggle dynamics using Lotka-Volterra predator-prey equations, with the workers ironically performing the role of the “predators” in the model as their wages fluctuate over the course of the cycle.

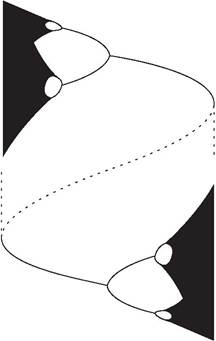

Pohjola (1981) showed that a discrete version of this model could produce chaotic dynamics and Soliman (1996) shows that it can also lead to fractal basin boundaries between multiple basins of attraction.Goodwin’s (1951) version of the nonlinear accelerator has also been shown capable of being modified to produce dynamics that exhibit both catastrophic discontinuities along with chaotic dynamics in a phenomenon dubbed “chaotic hysteresis” initially by Abraham and Shaw (1987). More particularly Puu (1997: ch. 8) posits that the investment function be non-monotonic rather than merely nonlinear. An example of chaotic hysteretic dynamics can be seen in Figure 4 that holds for certain parameter values of the Puu model, with the horizontal axis being output and the vertical one being the change of output.

Another route by which complex endogenous dynamics can arise in economic models is through the self-organized criticality phenomenon (Bak 1996). Bak et al. (1993) present such a model, which depends on a lattice structure of multiple pathways and stages of production in a sandpile model. This can allow a Gaussian distribution of exogenous shocks (sand dropping on the sandpile) to generate non-Gaussian distributions of final outcomes.

Figure 4 Chaotic hysteresis in a Puu nonlinear accelerator model

Unsurprisingly adding a financial sector to many of these models simply increases the likelihood that one can observe some form of complex dynamics. Among those finding chaotic dynamics include Foley (1987), Woodford (1989), and Delli Gatti et al. (1993). A variation on these models involves the role of speculative bubbles in the financial sector, which harks back to our earlier discussions of the role that such can play in macroeconomic dynamics going back to Mill and even to the origins of economic dynamics discussions with Cantillon. This links to more modern post-Keynesian concerns such as those involving financial fragility following the work of Minsky (1986). That bubbles might be chaotic was first shown by Day and Huang (1990), and Keen (1995) has shown this in the context of a model more directly based on Minsky.